Last week, the stock markets experienced a notable rally, driven by a combination of the Federal Reserve's decision to cut interest rates and growing investor optimism following the recent U.S. elections. With the possibility of a Republican-controlled Senate and executive branch, investors are hopeful about the potential for pro-business policies and fiscal stimulus moving forward. The House of Representatives, still undecided, is adding a bit of uncertainty, but overall, the mood is cautiously upbeat.

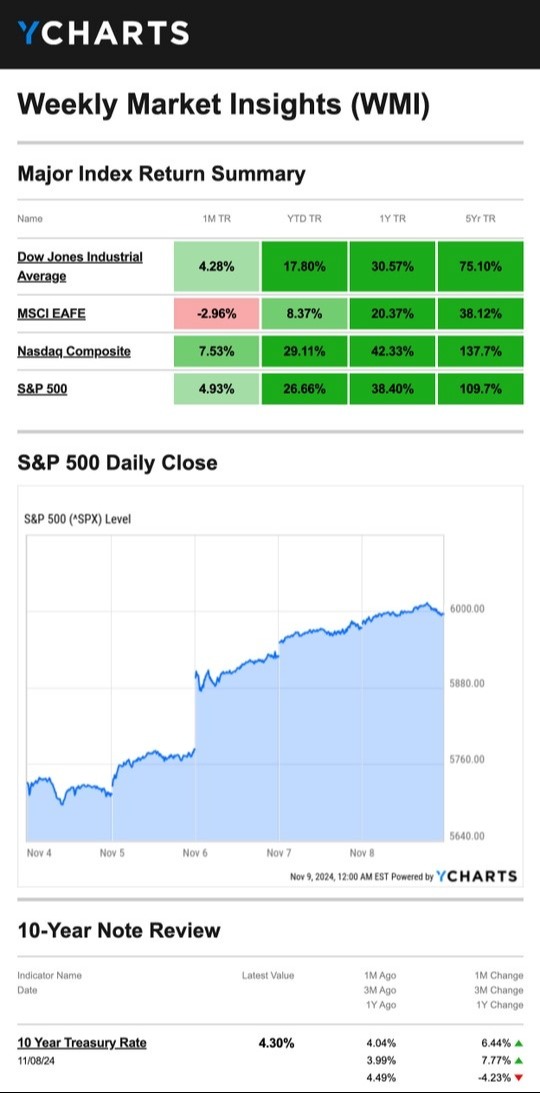

In the U.S., the Standard & Poor’s 500 Index surged 4.65%, while the Nasdaq Composite Index led the charge with a 5.74% gain. The Dow Jones Industrial Average also saw a strong uptick, rising 4.61%. Meanwhile, the MSCI EAFE Index, which tracks developed international markets, remained largely flat, dipping just slightly by -0.02%.

For our Canadian friends, the markets on this side of the border were also reflecting a sense of optimism. The S&P/TSX Composite Index, which tracks Canadian equities, posted solid gains as well. Resource stocks, particularly in the energy and materials sectors, helped to fuel the Canadian market's rise, as oil prices continued their upward momentum, spurred on by global economic expectations and OPEC+ production cuts.

Canada's economy, closely tied to the U.S., is benefiting from the same positive sentiment, but there's also a specific focus on how Canadian policy could align with potential shifts in U.S. trade and tax laws under a new administration. With uncertainty surrounding the House, many are also keeping a close eye on the Canadian dollar, which could see more volatility as the political landscape continues to evolve south of the border.

Stocks Extend Rally on Election News

It was a bit of a bumpy ride for stocks at the start of the week, with investors on edge as they waited for both the election results and the Federal Reserve's decision on interest rates. There was a lot of uncertainty hanging in the air, and markets didn’t have a clear direction at first.

But once Election Day arrived, the mood shifted. As polling places closed, stocks surged across the board, buoyed by optimism as the results started to roll in. The following morning, when the election was called early, the markets responded with enthusiasm, opening higher and gaining momentum throughout the day. The 10-year Treasury yield also dipped to 4.307%, signaling some relief on the bond side.

Then came Thursday, and with it, more good news. Stocks opened strong, but the real boost came after the Federal Reserve announced its second consecutive interest rate cut. Investors seemed reassured, especially after a report showed a solid 2.2% rise in third-quarter productivity—another positive signal for the economy.

By the end of the week, things had taken a dramatic turn for the better. The S&P 500 reached a milestone, crossing the 6,000 mark for the first time, and the Dow hit 44,000—a major psychological threshold. While both indexes ended the week slightly below those peaks, they still wrapped up their best week in over a year. It was a week of rallying highs, uncertainty, and relief, leaving investors feeling much more optimistic as they looked ahead.

Source: YCharts.com, November 9, 2024. Weekly performance is measured from Monday, November 4, to Friday, November 8. TR = total return for the index, which includes any dividends as well as any other cash distributions during the period. Treasury note yield is expressed in basis points.

He’s Back - What Can We Expect From Trump’s Second Term?

Predicting exactly how things will unfold with Trump is always a bit of a gamble. But looking at what we know so far, here’s a quick rundown of what a second Trump presidency could mean for both the U.S. and Canada:

1. Canada’s Economy:

Trump has made it pretty clear that he’s not a fan of trade deals as he believes it gives Canada an unfair advantage. Back in 2018, he imposed a hefty 25% tariff on Canadian steel, which led to Canada retaliating with tariffs of its own on American goods—from ketchup to scented candles. Now, Trump is threatening to slap 10–20% tariffs on all imports into the U.S. If that happens, it could cost Canada’s economy an estimated $30 billion a year and weigh down our GDP. On top of that, if Canada retaliates again, consumers could end up paying the price, as tariffs raise the cost of imports and could even drive inflation higher. Canadian officials are probably hoping for some savvy diplomacy to keep at least some of these tariffs from affecting us too much.

2. America’s Economy:

On the U.S. side, many economists agree that Trump’s proposed tariffs could hurt growth and even spark inflation in the short term. But investors are betting that some industries, particularly steel and aluminum, will actually benefit. The idea is that higher tariffs could strengthen U.S. manufacturing, which is already showing signs of improvement. Then there’s Trump’s tax plan—he’s promised sweeping cuts to income taxes, corporate taxes, and even taxes on overtime pay. While this could give the economy a short-term boost, it would also balloon the U.S. deficit, which could create a whole new set of challenges down the road. And if Trump follows through on his plan to deport millions of immigrants, that could create a labor shortage and push inflation even higher. Another wild card: If access to reproductive health care is further restricted, it could push women out of the workforce, further tightening the labor market.

3. Global Impact:

Trump has a long-standing beef with countries like Mexico and China, and he’s already threatening tariffs in the 60–100% range. For many countries, especially those in emerging markets, that’s a cause for concern—just last week, indexes tracking developing economies dropped by 2.5%. On the flip side, countries like Cambodia and Vietnam might actually benefit if companies decide to shift manufacturing out of China to avoid sky-high tariffs.

This Week: Key Economic Data

Tuesday: Fed Officials Neel Kashkari and Patrick Harker speak.

Wednesday: Consumer Price Index. Fed Officials Lorie Logan, Alberto Musalem, and Jeffrey Schmid speak. Treasury Buyback Announcement.

Thursday: Producer Price Index. Fed Chair Jerome Powell speaks. Weekly Jobless Claims.

Friday: Retail Sales. Industrial Production. Import and Export Prices. Business Inventories.

Source: Investors Business Daily - Econoday economic calendar; November 8, 2024

The Econoday economic calendar lists upcoming U.S. economic data releases (including key economic indicators), Federal Reserve policy meetings, and speaking engagements of Federal Reserve officials. The content is developed from sources believed to be providing accurate information. The forecasts or forward-looking statements are based on assumptions and may not materialize. The forecasts also are subject to revision.

This Week: Companies Reporting Earnings

Tuesday: The Home Depot, Inc. (HD), Shopify Inc. (SHOP), Spotify Technology (SPOT)

Wednesday: Cisco Systems, Inc. (CSCO)

Thursday: The Walt Disney Company (DIS), Applied Materials, Inc. (AMAT), Brookfield Corporation (BN)

Source: Zacks, November 8, 2024.

Companies mentioned are for informational purposes only. It should not be considered a solicitation for the purchase or sale of the securities. Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost. Companies may reschedule when they report earnings without notice.

“Many men go fishing all of their lives without knowing that it is not fish they are after.”

- Henry David Thoreau

What common English-language word becomes shorter when you make it longer?

Last week’s riddle: I am only one syllable long and too heavy for one person to lift, but if you reverse me, I am not. What am I?

Answer: A ton.

Our teams Alice and Wonderland themed Halloween costumes. Don't ask me if I am TweedleDee or TweedleDum... :)

Footnotes and Sources

- The Wall Street Journal, November 8, 2024

- Investing.com, November 8, 2024

- CNBC.com, November 4, 2024

- CNBC.com, November 5, 2024

- The Wall Street Journal, November 6, 2024

- The Wall Street Journal, November 7, 2024

- MarketWatch.com, November 7, 2024

- The Wall Street Journal, November 8, 2024

- The Wall Street Journal, November 7, 2024

- IRS.gov, January 30, 2024

- American Heart Association, July 24, 2024

Investing involves risks, and investment decisions should be based on your own goals, time horizon, and tolerance for risk. The return and principal value of investments will fluctuate as market conditions change. When sold, investments may be worth more or less than their original cost.

The forecasts or forward-looking statements are based on assumptions, may not materialize, and are subject to revision without notice.

The market indexes discussed are unmanaged, and generally, considered representative of their respective markets. Index performance is not indicative of the past performance of a particular investment. Indexes do not incur management fees, costs, and expenses. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results.

The Dow Jones Industrial Average is an unmanaged index that is generally considered representative of large-capitalization companies on the U.S. stock market. Nasdaq Composite is an index of the common stocks and similar securities listed on the NASDAQ stock market and is considered a broad indicator of the performance of technology and growth companies. The MSCI EAFE Index was created by Morgan Stanley Capital International (MSCI) and serves as a benchmark of the performance of major international equity markets, as represented by 21 major MSCI indexes from Europe, Australia, and Southeast Asia. The S&P 500 Composite Index is an unmanaged group of securities that are considered to be representative of the stock market in general.

U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid. Fixed income investments are subject to various risks including changes in interest rates, credit quality, inflation risk, market valuations, prepayments, corporate events, tax ramifications and other factors.

International investments carry additional risks, which include differences in financial reporting standards, currency exchange rates, political risks unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility.

Please consult your financial professional for additional information.